Is The Correction In OKTA Over? After falling more than 30% from 2021's high, it looks like the correction in OKTA (NASDAQ: OKTA) could be over. OKTA, a leader in identity protection and 0-Trust security, reported...

By Thomas Hughes •

This story originally appeared on MarketBeat

Blowout Results Spark Volatility In OKTA Shares

After falling more than 30% from 2021's high, it looks like the correction in OKTA (NASDAQ: OKTA) could be over. OKTA, a leader in identity protection and 0-Trust security, reported a blowout quarter marred by only one thing. The company's margins contracted and reverted to a net loss but there is a mitigating factor. The loss is associated with an aggressive ramp in R&D and marketing that should result in accelerated sales in future quarters. While revenue jumped high double-digits over the past year spending on both R&D and marketing more than doubled. With others in the hyper-growth 0-Trust community doing the same we think this is a good move indeed.

"Our strong third-quarter results reflect the continued shift to Identity-First architectures and the critical adoption of Zero Trust security environments, which are both propelling our market-leading position," said Todd McKinnon, Chief Executive Officer and co-founder of Okta. "We're maintaining the momentum of both Okta and Auth0 and are making great progress on the integration. We're already seeing early success cross-selling into each other's customer bases and are on our way to capturing more of the massive identity market faster together."

Mixed Results Send OKTA Lower, Then Higher

OKTA, Inc had a strong quarter with only one blemish to mar the results. The $350.68 million in net revenue is not only up 61.3% over last year but it also beat the consensus estimate by 700 basis points. Revenue gains are driven by a 63% increase in subscriptions coupled with a 32% increase in Professional services. Subscriptions are the company's bread & butter and account for more than 96% of the net. It is also worth noting that 24 of 25 analysts raised their target in the month before the results were released so the bar to clear was very high indeed.

Moving down, the company reported a slight 200 basis point decline in gross margin to 71% that is, ultimately, better than expected. The real bad news and, again, it's not really that bad, is that the operating margin fell into negative territory and exceeded the analyst's expectations. At the GAAP level, the company posted a loss of $1.44 per share to exceed the consensus by $0.20 but that gap is easily made up for by adjustment factors. On an adjusted basis, the company reported a loss of only $0.07 to beat expectations by $0.16 and set it up for outperformance next quarter as well.

The company is expecting business strength to continue into the end of the year. Revenue is projected to grow at least $8 million sequentially or 2.3% and exceed the Marketbeat.com consensus estimate by at least $3 million. For the full year, revenue should come in better than $1.275 million or $0.025 million ahead of expectations with earnings in even better positions. The company is expecting the FY adjusted loss to be only $0.52 to $0.53 compared to the consensus of $0.72.

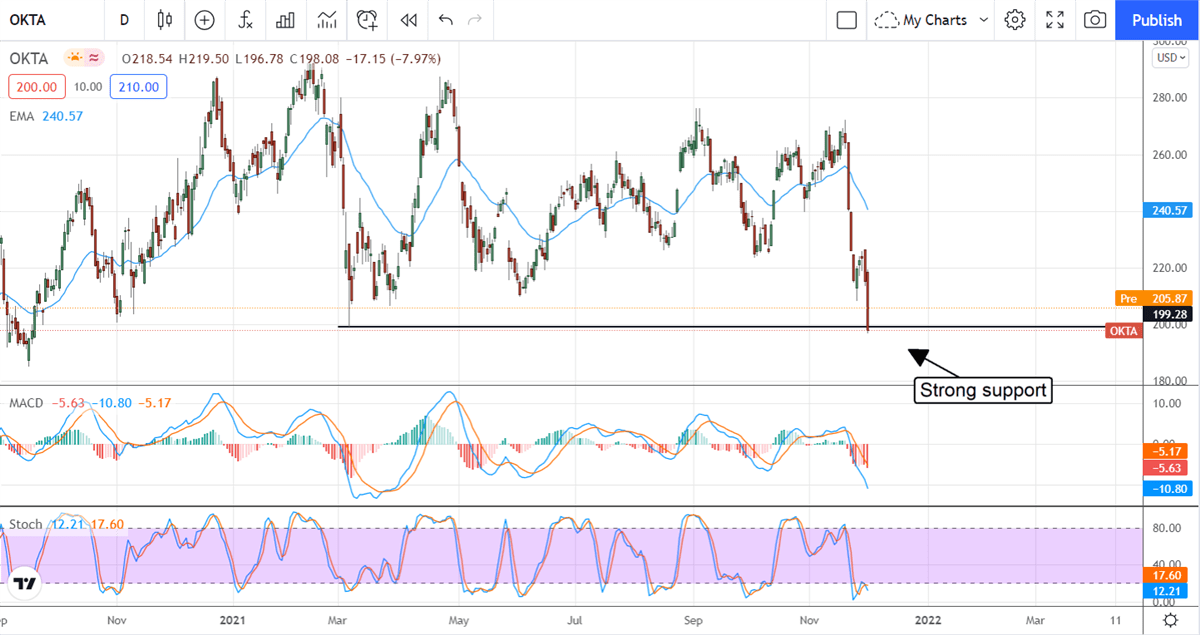

The Technical Outlook: OKTA Confirms Support

Shares of OKTA saw some volatility in the wake of the Q3 earnings report but are trading higher in premarket trading now. The move confirms support at the $199 level and the bottom of an 18-month trading range so we view it as a strong signal. Assuming the market carries through on this move, we see shares of OKTA moving back up to the top of the range near $280. This is coincident with the Marketbeat.com analyst consensus price target of $289 and there is positive activity among the analysts. At least 6 sell-siders have come out with commentary to include several lowered targets but all pointing to higher share prices. The high price target of $320 was also reiterated by Needham.