Can Uber (NYSE: UBER) Get Back On Track?

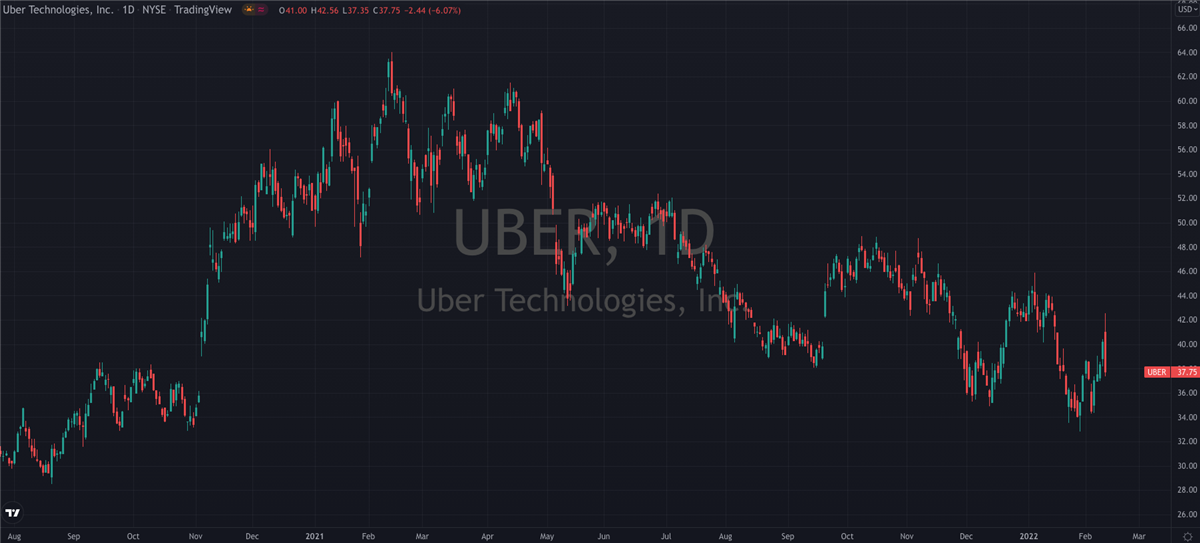

Shares of ride hailing titan Uber (NYSE: UBER) have been under significant pressure since this time last year, having had their price cut almost in half.

This story originally appeared on MarketBeat

Shares of ride hailing titan Uber (NYSE: UBER) have been under significant pressure since this time last year, having had their price cut almost in half. This time last year they were trading at all time highs, but it’s been death by a thousand cuts for investors since. For a few days last month they were even trading below their 2019 IPO price, but there are a few reasons to think a turnaround might be on the cards.

For starters, their Q4 earnings report, released this past Wednesday, landed a solid beat on what analysts had been expecting. Revenue came in at $5.8 billion, almost $500 million higher than the consensus, and showed year on year growth of 82%. Bottom line EPS was also hot, and at $0.44 was well ahead of the -$0.33 loss that had been expected.

Strong Results

Investors were also pleased to see that the gross bookings figure was up 51% year on year, and at the high end of the guidance range. CEO Dara Khosrowshahi summed up the report by saying”our results demonstrate just how far we’ve come since the beginning of the pandemic. In Q4, more consumers were active on our platform than ever before, Delivery reached Adjusted EBITDA profitability, and Mobility Gross Bookings approached pre-pandemic levels. While the Omicron variant began to impact our business in late December, Mobility is already starting to bounce back, with Gross Bookings up 25% month-on-month in the most recent week.”

This optimistic outlook was added to by CFO Nelson Chai, who made the point that “we outperformed our quarterly guidance and delivered $540 million of Adjusted EBITDA improvement compared to Q4 of last year. Moving forward, we are poised to continue to grow at scale while expanding profitability.”

Uber shares popped in the aftermath of the report, and at one point yesterday were up as much as 30% from January’s multi-month low. But the wind was taken from the sales by the company’s investor day yesterday, where Chai offered forward guidance that was softer than what Wall Street had been looking for. Specifically, he said that the company expects its adjusted earnings to reach $5 billion by 2024, with gross bookings of $165 billion to $175 billion. According to Reuters however, analysts surveyed by Refinitiv had expected the company to generate $5.7 billion in adjusted earnings in 2024.

Having been up 5% in that session alone, they quickly hit reverse and actually ended the session down 6%. This was a bit unfortunate, as the day after your earnings are released is an interesting time to schedule an investor day. You’ll often find them dotted around the middle of a quarter, where a company can provide fresh guidance or news that acts as a catalyst to shares when they might be losing some post-earnings steam. But whatever their reasoning, the end result was that shares were back trading to their pre-earnings levels by the time the bell rang to end yesterday’s session. They were flat in Friday’s pre-market session so maybe there’s some hope yet that they’ll catch a bid into the weekend.

Getting Involved

Because ultimately, there’s more to like about Uber than dislike right now, as Wedbush summed up yesterday. Analyst Ygal Arounian said in a note that “we would characterize this quarter and initial guidance as a big step in the right direction for Uber which should give investors incremental confidence in the recovery story thesis for 2022″. Uber’s Outperform rating was maintained, as was their $57 price target, which suggests there’s massive upside to be had in the region of 50% from current levels. This should be more than enough to entice investors in from the sidelines, as Arounian feels that the past quarter was strong and showed what a profitable version of Uber can do.

To be sure, risks remain to the downside, and Uber shares must break through the downtrend that’s been in place for a year if they’re to have any hope of staging a fightback. But this company is growing revenues at 80% year on year, and just smashed analyst expectations. Sure, they might have guided a little light on forward revenue, but it’s not unreasonable to think the past year’s selling has more than accounted for that.

Shares of ride hailing titan Uber (NYSE: UBER) have been under significant pressure since this time last year, having had their price cut almost in half. This time last year they were trading at all time highs, but it’s been death by a thousand cuts for investors since. For a few days last month they were even trading below their 2019 IPO price, but there are a few reasons to think a turnaround might be on the cards.

For starters, their Q4 earnings report, released this past Wednesday, landed a solid beat on what analysts had been expecting. Revenue came in at $5.8 billion, almost $500 million higher than the consensus, and showed year on year growth of 82%. Bottom line EPS was also hot, and at $0.44 was well ahead of the -$0.33 loss that had been expected.

Strong Results

Investors were also pleased to see that the gross bookings figure was up 51% year on year, and at the high end of the guidance range. CEO Dara Khosrowshahi summed up the report by saying”our results demonstrate just how far we’ve come since the beginning of the pandemic. In Q4, more consumers were active on our platform than ever before, Delivery reached Adjusted EBITDA profitability, and Mobility Gross Bookings approached pre-pandemic levels. While the Omicron variant began to impact our business in late December, Mobility is already starting to bounce back, with Gross Bookings up 25% month-on-month in the most recent week.”

This optimistic outlook was added to by CFO Nelson Chai, who made the point that “we outperformed our quarterly guidance and delivered $540 million of Adjusted EBITDA improvement compared to Q4 of last year. Moving forward, we are poised to continue to grow at scale while expanding profitability.”