A Modern Retirement Mindset: Elevate Meaning and Purpose By Becoming ‘Job Optional’

With the right framework, you can stop worrying about what’s next and focus on what’s here today.

Opinions expressed by Entrepreneur contributors are their own.

This article was written by Casey Weade, CFP®, author of the Wall Street Journal bestseller, Job Optional, and president of the retirement planning firm, Howard Bailey Financial, Inc.™

A successful retirement plan doesn’t begin with how much money is in your bank account. It begins with you – your purpose. Truth be told, the traditional idea of retirement from days past is long gone. You’re living longer, which means you have more time to fill and greater opportunity to make an impact in the world.

While strategic financial planning is important, aligning your money with your life’s meaning and purpose plants the roots for a truly fulfilling retirement. I realized this after achieving financial independence early in my life. I reached the financial finish line, but felt disillusioned. Why continue working if it wasn’t for the money? I needed to make a shift that was in line with my gifts.

Related: 4 Ways to Save for Retirement Without a 401(k)

I realized I could leverage my talent to help others use their wealth for elevating meaning and purpose in their own lives. By uncovering a financial framework that allowed me to reach “Job Optional” status, I could show others how to get there financially too. And more importantly, I could help guide them through how to make a bigger impact in the world than when they arrived.

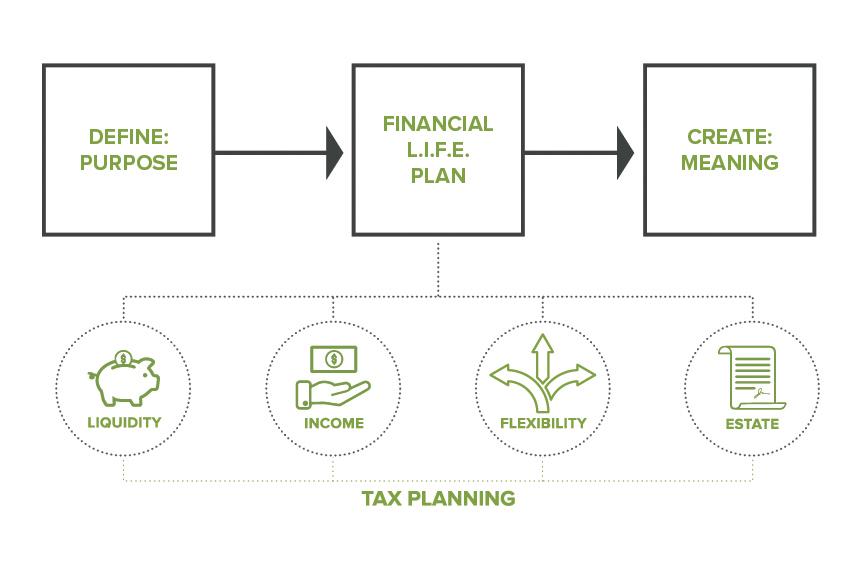

I found that no matter what path you choose after “arriving”, if you are intentional with your second act, your impact will always be largest in the lives of others. I call this financial formula the “Retire With Purpose Framework”, and I utilize the concept as a guide to help others live and retire with money AND purpose. Your purpose will guide what I call your “Financial L.I.F.E plan”. It’s truly customized to you, and includes four main pillars: Liquidity, Income, Flexibility, Estate; Plus, the all-encompassing aspect of tax planning.

Here’s how it looks.

Image credit: Casey Weade

Liquidity

Many financial advisors believe you should keep as little cash as possible — that’s how they make money. But I find the happiest retirees have the largest cash balances, not the biggest brokerage accounts.

Knowing you’re prepared for the unexpected provides confidence. Perhaps your furnace or car breaks down, you want to help a struggling family member, or your dream trip becomes available sooner than planned. When you have safe, accessible funds, you have a plan for emergencies and opportunities.

While experts recommend having at least three months’ worth of expenses saved for emergencies, that should be a bare minimum. And regardless of where you keep this financial safety net, what matters most is that the money is there when you need it.In other words, don’t put it at risk or tie it up. You might not make much interest, but that’s okay. You’ve already made it to the finish line. It’s about peace of mind at this time, not growth at all costs.

Income

Without income, there is no retirement. This might be the most important part of your retirement strategy, as you shift from the accumulation stage to creating consistent, reliable income that you can’t outlive.

The best financial advice I’ve ever received was this: it’s not about how much money you make, but how much you keep. This is especially true in retirement.

Retirement income strategies are nearly endless but should be customized to your unique, financial situation. Most affluent retirees don’t spend nearly as much as they could, because, without a strategy, they’re always concerned about the next stock market crash.

Related: 6 Reasons to Pursue Entrepreneurship in Retirement

A REAL income strategy prepares for the best, but plans for the worst. In my book, “Job Optional”, I share a number of different strategies with varying degrees of risk and reward. There’s no such thing as a perfect income strategy. You simply need to find the perfect one for you personally, and that begins with a foundation in education.

Flexibility

The unknown is inevitable, and when things change, we need to be prepared to adapt. Unprecedented events regularly occur in financial markets and our personal lives, requiring adjustments. It could be as simple as wanting to relocate near your grandkids in a more expensive neighborhood, or as precarious as hyperinflation.

Inflation is the one aspect that may stand out the most to you. It could even be one of your biggest retirement concerns. However, inflation may not impact you as much as you think when in retirement. Financial planners often project a standard three percent inflation rate that nearly doubles your expenses over 20 years of retirement.

Dr. David Blanchett, head of retirement research at the global financial services firm Morningstar, shared his research on my podcast explaining that these projections don’t typically stand up to reality. Retirees’ expenses typically decline over time, balancing out the impact of inflation. This I can personally attest to after working with thousands of retirees over the years.

Now, this doesn’t mean the future will be the same as the past. You need a diversified portfolio of funds, positioned for long-term growth to provide the flexibility to adapt to an unknown future, composed of investments that profit from increasing prices, like stocks, real estate, and commodities.

Estate

Having an estate plan provides peace of mind that your assets will be distributed according to your wishes upon your passing. It includes establishing basic estate planning documents and beneficiaries, but it also goes beyond that, as it protects your heirs from future tax pitfalls, and prepares your estate for major healthcare expenses.

According to the 2020 Genworth Cost of Care Survey, the cost of a semi-private room in a nursing home facility averaged $7,756 per month, and seven out of ten people age 65 will require some form of long-term care before death.

Where would this leave your spouse if you had long-term care expenses in the six figures? You can self-insure or purchase insurance coverage, but at minimum, evaluating medical expenses as a part of your planning is crucial.

Most retirees’ assets are tied up in tax-deferred retirement plans. These are taxed at your non-spouse beneficiaries’ highest marginal tax rate upon death — and due to the SECURE Act of 2019, must be distributed within ten years of death.

You may want to evaluate Roth conversions and life insurance as a potential tax-free legacy solution, and more intensive estate planning to avoid death taxes for large estates.

Tax planning

You will be paying taxes throughout your life, and as such, tax planning should be weaved throughout your entire “L.I.F.E. Plan,” not just as part of your estate plan.

One of my favorite quotes is, “You should not be spending money on money you’re not spending.” Think about these different buckets of money you have allocated for varying purposes. Which one makes the most sense to be generating on-going tax liability? It’s your income bucket, of course, because it’s the only one you should be spending!

Perhaps this means reallocating your liquid funds to tax-deferred or tax-free tools and/or accounts. Maybe this is reallocating your dividend stocks to a Roth IRA, and the growth stocks to your taxable accounts. For your income dollars, it may mean blending tax-deferred, taxable and tax-free accounts to maintain a certain taxable income to avoid Social Security taxes or Medicare premium penalties. It could even mean leveraging various trust structures as part of your estate plan.

Effective tax planning means you and your heirs keep more of your hard-earned dollars, allowing you to spend more today and leave more behind tomorrow.

There’s no silver bullet

The perfect investment doesn’t exist, but if you can identify the specific purpose for your life savings, you can find the most efficient way of getting there. It requires time, planning, and an understanding by both you – and a financial professional – that it’s personal.

Image credit: Casey Weade

You didn’t get here overnight, so take your time in implementing a written strategy. Our team does this using a four-step process, beginning with a discovery visit, followed by a strategy, implementation and delivery visit.

The discovery visit should be all about you: Who you are, what drives you, and what retirement means to you. Your strategy visit should outline any gaps in your financial plan, as well as options. Once you’ve selected what’s right for you, dive into execution in the implementation visit, followed by a review of a finalized written document in the plan delivery.

Financial peace of mind is priceless. Once you reach “Job Optional” status, you’ll be amazed by what changes in your life. It’s time to stop worrying about what’s next, and focus on where life is actually happening, right now.

Read Job Optional to learn more about the “Retire With Purpose Framework” or catch Casey Weade’s “Retire With Purpose” podcast, TV and radio shows for guidance on maximizing your financial efficiency.

EDITOR’S NOTE: This article expresses the views and opinions of an individual and is not a substitute for professional financial advice. Do your own research and consult your own financial adviser.

This article was written by Casey Weade, CFP®, author of the Wall Street Journal bestseller, Job Optional, and president of the retirement planning firm, Howard Bailey Financial, Inc.™

A successful retirement plan doesn’t begin with how much money is in your bank account. It begins with you – your purpose. Truth be told, the traditional idea of retirement from days past is long gone. You’re living longer, which means you have more time to fill and greater opportunity to make an impact in the world.

While strategic financial planning is important, aligning your money with your life’s meaning and purpose plants the roots for a truly fulfilling retirement. I realized this after achieving financial independence early in my life. I reached the financial finish line, but felt disillusioned. Why continue working if it wasn’t for the money? I needed to make a shift that was in line with my gifts.