Buy These 2 Tech Stocks on the Dip

We’ve seen a major correction in growth stocks over the last few months. This is clearly setting up a buying opportunity in a handful of high-quality names. Taylor Dart breaks down why you should consider adding Netflix (NFLX) and Roblox (RBLX) on the dip.

This story originally appeared on StockNews

It’s been a volatile 4-month stretch for the Nasdaq Composite (QQQ), and while there have been a few notable winners, performance has been bifurcated in the tech space. Fortunately, this correction has allowed the index to unwind some of its overbought condition, pushed some names to much more reasonable valuations, and made it less difficult to uncover names that are under accumulation.

While the medium-term upside for the Nasdaq Composite is less clear given that we continue to have a high level of complacency in the overall market, two names do look intriguing. One is a new potential market leader, with the other being a former leader that’s now trading at a compelling valuation. Let’s take a closer look at both stocks below:

(Source: TC2000.com)

Roblox (RBLX) and Netflix (NFLX) don’t have much in common given that they come from separate industry groups, with Roblox being in the Computer Software/Gaming Group and Netflix being in the Leisure, Movies & Related Group. However, the one trait these companies do share is an exceptional product or service attracting and maintaining a massive amount of daily active users or subscribers, in NFLX’s case. For Roblox, the company has seen daily active users [DAUs] soar to 42.1MM as of Q1 2021, a more than 63% compound annual growth rate since Q1 2019.

While NFLX’s high growth days are behind us and both companies are in very different stages of their growth cycle, recent pessimism surrounding NFLX’s best days being over has left the stock at a very attractive valuation. Let’s begin with the investment case for RBLX:

Roblox is likely a less familiar name for most investors, given that the company just went public in March. However, for parents worldwide, Roblox might be a household name by now, with an army of kids logging a massive amount of hours on Roblox each day. For kids under 13, hours spent on Roblox soared to 4.8BB in Q1 2021 alone, with total hours (under age 13 & over age 13) coming in at 9.7BB.

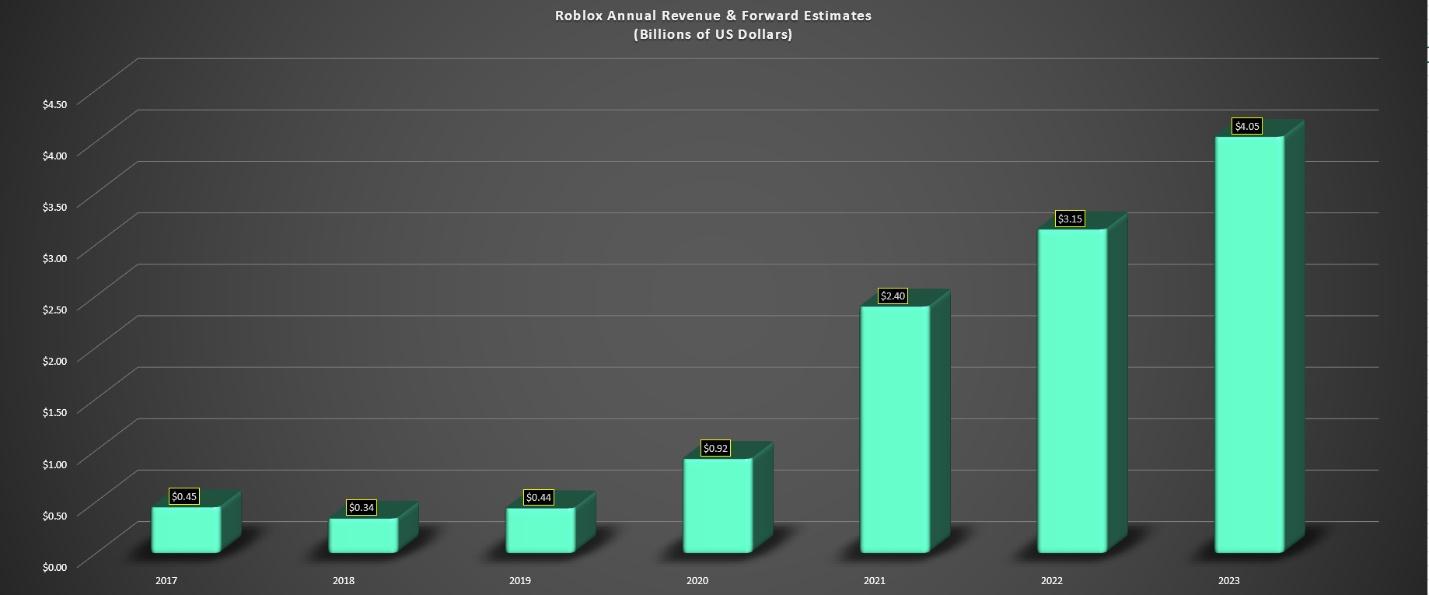

This represents an astounding 80% compound annual growth rate since Q1 2019, showing that hours of engagement are increasing at a faster pace than DAUs, a very positive sign. Not surprisingly, this has led to triple-digit revenue growth, with Q1 2021 revenue coming in at $387MM, up 140% year-over-year.

(Source: Company Filings, Author’s Chart)

If we look at revenue projections going forward, revenue growth rates are projected to remain quite robust, with FY2021 revenue estimates of $2.4BB and FY2023 estimates of $3.15BB. This would translate to an 85% compound annual growth rate if estimates are met, making RBLX one of the highest growth names in the market currently.

Despite these incredible growth rates, RBLX trades at just 22x FY2021 sales at a market cap of $53BB and less than 17x FY2023 sales. Given that the highest growth companies in their earlier years of growth can easily justify a forward price to sales ratio above 30, there looks to be a solid upside for RBLX, with a fair value for the stock well above $120.00 per share.

(Source: TC2000.com)

If we look at RBLX’s technical picture, it’s very impressive, with the stock racing to new highs ahead of the general market and clearly showing it’s a market leader. This strong breakout on high volume suggests that funds & institutions might be accumulating the stock here, increasing the probability that any pullbacks will be buyable. While I wouldn’t be in a rush to chase the stock above $95.00 per share, I would view any pullbacks to the breakout level at $84.00 as low-risk buying opportunities.

Pullbacks to this level would leave the stock with more than 40% upside to a fair value of $120.00 and leave the stock short-term oversold.

Moving over to Netflix, the company just came off a weaker quarter than most were expecting. However, the situation is reminiscent of Google two years ago when the stock was underperforming its peers due to a couple of misses despite strong double-digit annual EPS growth on the horizon.

Google has since become the leader among the FAANG group by a wide margin, and I would expect NFLX to see strong share-price performance ahead once investors wake up to just how much free cash flow the company is generating.

While competition is an issue for NFLX, the amount of consumers cutting cable for streaming options continues to grow. This suggests that even if NFLX does lose some market share, its potential to grow is not impeded, given that there’s a growing pool of potential subscribers. So, even though competition talk remains rampant and most investors weren’t elated with only 24% growth year-over-year in sales to $7.2BB, this pessimism might be creating a buying opportunity.

This is because NFLX is becoming a growth at a reasonable price stock after this pullback, trading at just 37x FY2022 earnings estimates and 28x FY2023 earnings estimates. For a company with a projected compound annual EPS growth of 46% since FY2018 ($17.77 vs. $2.68), the stock is nearing an attractive entry point.

(Source: YCharts.com, Author’s Chart)

If we assume a fair earnings multiple of 45 on FY2022 earnings, NFLX’s fair value comes in at $672.00 per share, representing more than 30% upside from current levels. If we use FY2023 estimates of $17.77 and a lower multiple of 40 to account for risk due to higher competition, fair value comes in at $710.80 per share. Therefore, at a share price of $502.00, I would view any further weakness as a buying opportunity, and I may look to add to my position started at $371.00 if we see a dip below $470.00.

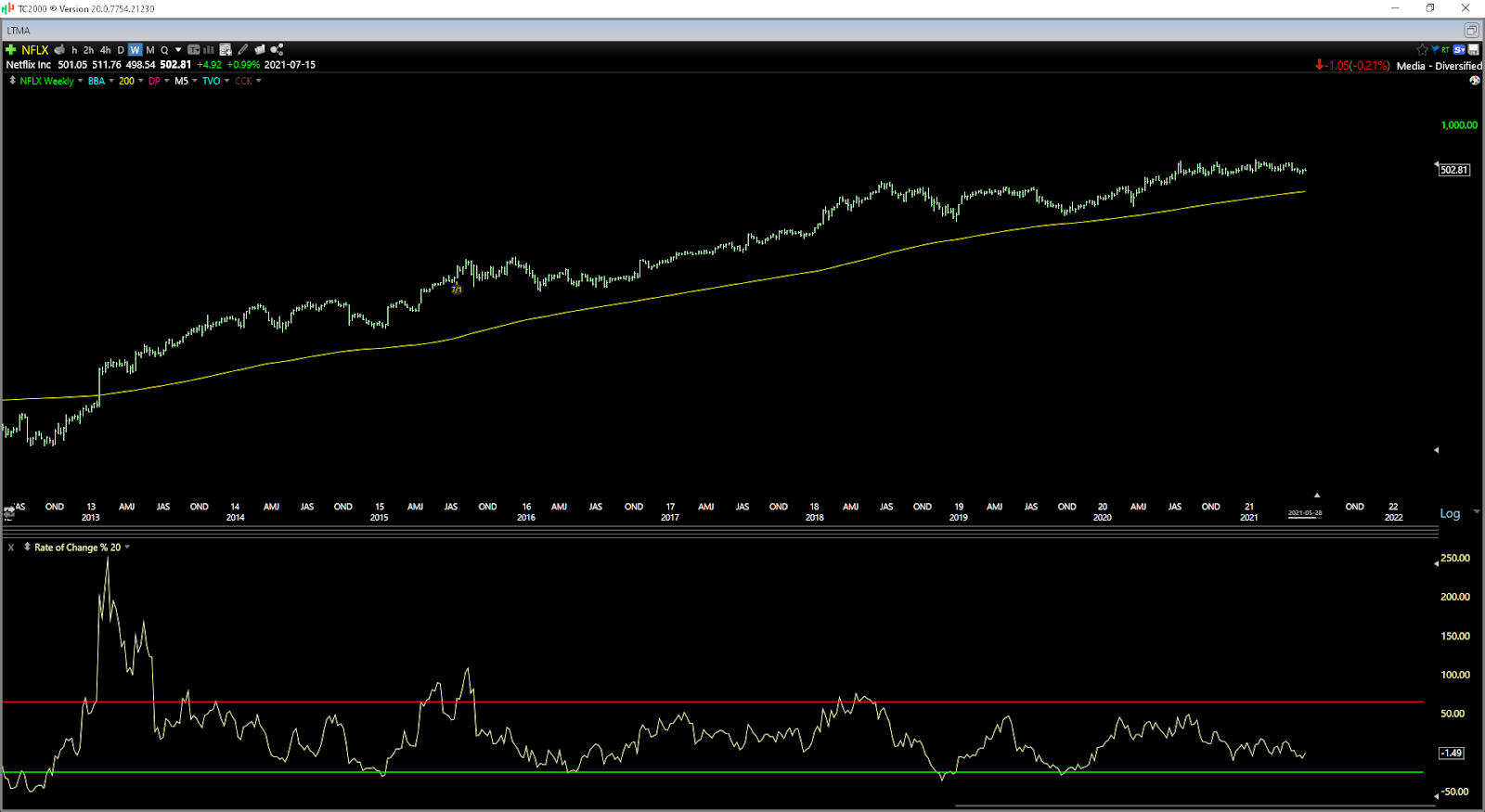

(Source: TC2000.com)

Moving to the technical picture, NFLX is now quite at deeply oversold levels but is getting much closer to these levels after the recent correction. As shown above, pullbacks close to the green line have been buying opportunities, with the stock typically gaining at least 50% in less than 12 months following these signals.

While we don’t have a deeply oversold signal yet, a pullback to $470.00 would likely satisfy, setting up the stock for strong upside going forward. This reinforces the view that further weakness should present a buying opportunity.

While the Nasdaq Composite continues to remain expensive, as does the S&P-500, which trades at a record price to sales metrics, RBLX and NFLX look like two decent names to buy on dips. If RBLX trades below $84.00, this will present a low-risk buying opportunity, and if NFLX dips below $485.00, I would view this as a low-risk area to start a position.

Obviously, there’s no guarantee we see further weakness in these names, but I believe they should be at the top of one’s shopping list if we do see further retracements.

Disclosure: I am long NFLX

Disclaimer: Taylor Dart is not a Registered Investment Advisor or Financial Planner. This writing is for informational purposes only. It does not constitute an offer to sell, a solicitation to buy, or a recommendation regarding any securities transaction. The information contained in this writing should not be construed as financial or investment advice on any subject matter. Taylor Dart expressly disclaims all liability in respect to actions taken based on any or all of the information on this writing.

NFLX shares were trading at $499.73 per share on Tuesday morning, down $3.08 (-0.61%). Year-to-date, NFLX has declined -7.58%, versus a 12.66% rise in the benchmark S&P 500 index during the same period.

Netflix (NFLX) is a part of the Entrepreneur Index, which tracks some of the largest publicly traded companies founded and run by entrepreneurs.

About the Author: Taylor Dart

Taylor has over a decade of investing experience, with a special focus on the precious metals sector. In addition to working with ETFDailyNews, he is a prominent writer on Seeking Alpha. Learn more about Taylor’s background, along with links to his most recent articles.

The post

Buy These 2 Tech Stocks on the Dipappeared first on

StockNews.comIt’s been a volatile 4-month stretch for the Nasdaq Composite (QQQ), and while there have been a few notable winners, performance has been bifurcated in the tech space. Fortunately, this correction has allowed the index to unwind some of its overbought condition, pushed some names to much more reasonable valuations, and made it less difficult to uncover names that are under accumulation.

While the medium-term upside for the Nasdaq Composite is less clear given that we continue to have a high level of complacency in the overall market, two names do look intriguing. One is a new potential market leader, with the other being a former leader that’s now trading at a compelling valuation. Let’s take a closer look at both stocks below: